Whenever interest rates are falling, senior citizens are always under stress to maintain their income, because their income from interest through fixed deposit is falling and that is their main source of income. NDA Govt which ended its tenure in 2004 was very sensitive to this issue and so they brought two schemes in their times, one was Senior Citizens Savings Schemes which worked through post office and banks and another was Varishtha Pension Bima Yojana which worked through Lic of India. Senior Citizens’s Savings Schemes is still working but Varishtha Pension Bima Yojana was closed later on.But in the Union Budget of 2014-15 our Finance Minister has proposed to revive it for a limited period of 15th August 2014 to 14th August 2015 for the benefit of Senior Citizens. Following are the features of the scheme.

Type of Plan: Varishtha Pension Bima Yojana is basically a annuity(pension) plan. But in this plan, investment has to be done lump sum and annuity (Pension) starts immediately based on the mode of pension selected.

Who Can Invest? : Any Individual can invest.

- Minimum Entry Age – 60 Years (completed) .

- Maximum Entry Age – No limit.

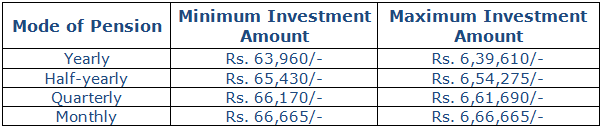

How much amount can be invested? :Investment in this scheme can be done only in lump sum mode. Following is the maximum and minimum limit of investment depending upon mode of pension opted by pensioner.

The investment should be rounded to nearest multiple of Rs.5/-.

Ceiling of maximum investment is for a family as a whole i.e. total amount of investment under all the policies issued to a family under this plan shall not exceed the maximum pension limit. The family for this purpose will comprise of pensioner, his/her spouse and dependents.

Mode of Pension Payment :Pension is paid either Monthly, Quarterly, Half Yearly, or yearly basis. First installment of pension will be paid after completion of one year (if yearly mode of pension is selected.), 6 months (if half yearly mode of pension is selected.) 3 months (if quarterly mode of pension is selected.), after one month (if monthly mode of pension is selected.)

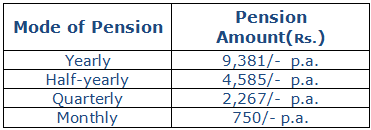

Sample Pension per Rs.100000/- of investment.

The pension rates for Rs.100000/- investment under different modes of pension amounts are as below:

- The pension installment shall be rounded off to the nearest rupee.

- Pension rates are not age specific.

Application Form : One can apply in form no. 470 (Rev) in LIC . Download Form

Tenure of Policy & Surrender Value :

- The pensioner can continue the policy for life time.

- The policy can be surrendered after 15 years and pensioner will get back his amount of investment.

- However, under exceptional circumstances, if the pensioner requires money for the treatment of any critical/terminal illness of self or spouse then the policy can be surrendered before the completion of 15 years and the Surrender Value payable shall be 98% of his investment.

Loan Facility:

- Loan facility is available after completion of 3 year of investment. The maximum loan that can be granted shall be 75% of investment amount.

- The rate of interest to be charged for loan amount would be determined from time to time by the LIC.

- Loan interest will be recovered from pension amount payable under the policy. The Loan interest will accrue as per the frequency of pension payment under the policy and it will be due on the due date of pension. However, the loan outstanding shall be recovered when the amount of investment is returned back on the death of Pensioner or at the time of surrender.

Tax Implications :

- No Deduction at the time of making investment.

- Pension received is taxable under the head income from other sources.

Conclusion :Varishtha Pension Bima Yojana offers an investment option for limited maximum amount of investment for senior citizens but assures guaranteed taxable return of around 9.30% p.a. for life time. I would recommend that those senior citizens who are investing in fixed deposit for the taxable interest income should give first priority to Varishta Pension Bima Yojna because right now because this provides better interest rate than Bank fixed deposits and guarantees this income for the life time of senior citizen where as in case of Bank fixed deposit at the time of renewal of the fixed deposit interest rate will change and interest income of senior citizen will fall.