In my last article we had discussed “What is HUF & How to create HUF?” In this article we will be discussing How to reduce your Tax Liability using HUF as a separate entity in the eyes of Income Tax Act.

♦ Separate Legal entity: HUF is a separate legal entity in the eyes of Income Tax Act. So for HUF separate Income Tax return has to be filled like we file in case of individual. Basic exemption limit for HUF are same as Individual so it works like a separate file. HUF also enjoys all the deductions and exemptions like Individual. One can make investment in different avenues and get benefits of Sec 80 C.

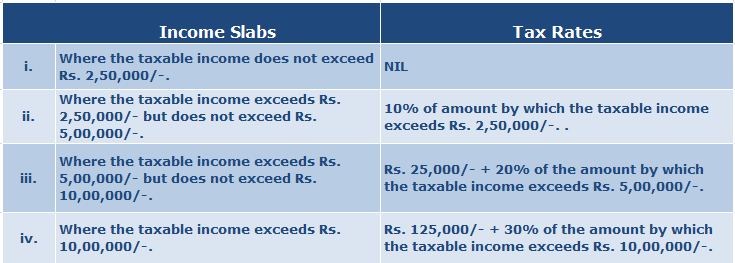

♦ Basic Exemption limit and Income Tax Slabs: As HUF is a separate legal entity. It enjoys the same benefit as an Individual and has separate Basic exemption limit as well as tax slabs same of an Individual. Following are the tax slabs of an HUF for Assessment Year 2015-16.

Surcharge: 10% of the Income Tax, where taxable income is more than Rs.1 crore. (Marginal Relief in Surcharge, if applicable)

EC & SHEC: 3% of the total of Income Tax and Surcharge.

♦ Deductions & Exemptions : All deduction of Section 80 and exemptions of Sec 10 of Income Tax Act available to an individual are also available to HUF.

♦ What HUF can do?

HUF Can be Proprietor: HUF can be proprietor of a firm. So one can start a firm where HUF is a proprietor and other members along with Karta are running that firm. Karta and other members can become employees of firm in which HUF is proprietor and earn salary income from the firm. This way the income can be split between HUF and members. A separate, different name can also be maintained for firm owned by HUF.

HUF can also own a Property : HUF can also own a property and receive rental income same as an individual can. So one can buy property in the ownership of HUF and receive rental income in HUF. This way one can shift the burden from individual to HUF.

HUF can claim benefits of section 24 under Income Tax Act: In case when HUF owns property it can claim benefit u/s 24 (a) of Income Tax Act for standard deduction of 30% from the rental income. Under this section rental income received by anyone gets standard deduction of 30% without spending anything. For example, if HUF received rent of Rs. 2 Lakhs p.a. from a property. Then in that case standard deduction would be Rs.60 thousand (30% of Rs. 2 Lakhs) so taxable rent would be Rs.1.4 Lakhs only.

Similarly, HUF can hold one self occupied property and claim benefit of Section 24(b) :

Under Income Tax Act, an individual can keep one residential premises as a self occupied property but if he purchases another residential premises then even though that premises is not rented and he is not receiving any rent from that, an amount equal to notional rent will be calculated and added in his income under the head income from other sources. For example if Mr.A possesses two houses in his own name and none of them is rented. Any one house at his choice can be treated self occupies and for other house a value equal to notional rent will be calculated and added in his total income. Here Mr.A can plan his affairs in such a way that another house can be bought in the name of Mrs. A from her own income and in such case she can also posses one more self occupied property. So even through husband and wife both are living in same house, for income tax purpose they can posses two different houses as self occupied for income tax purpose and nothing will be taxed as notional rent . But one step ahead from this situation, if they want to possess third house then in that case notional rent will be calculated and added in the income of owner.

Now if in above case if Mr.A and Mrs.A plan their financial affairs in such a manner that they buy third house in the ownership of Mr.A (HUF), then in such case third property will also become self occupied property and notional rent will not be added in the income of Mr.A, Mrs.A or Mr.A (HUF) if it is actually not given on rent. In this case the third house is also considered self occupied even though it is vacant and family is not living in that house because HUF can also hold one self occupied property under the income tax act.

In above case HUF can also take a home loan for property and claim benefit of deduction of interest paid on home loan up to Rs. 2 Lakhs form income of HUF under section 24(b) of the income tax act.

HUF can invest in different Securities : HUF can open demat account and invest in shares and also receive dividend income as well as capital gains. It can also invest in Mutual funds and fixed deposit or any other securities. HUF cannot open PPF account.

HUF can become Partner in a Partnership Firm :

- HUF can become partner in a partnership firm.

- HUF can receive interest on capital from Partnership Firm.

- HUF cannot receive salary as a working partner from Partnership Firm.

- But HUF can receive share in profit from Partnership Firm which is exempted from tax as Firm has already paid tax on it.

HUF can give Loan :

- HUF Can give loan to any one and receive interest for the same.

- So if you need some money for the purpose of using it in your business or profession, say for buying an instrument or machinery or anything related to your business or profession and you are taking loan from bank or any other agency and if you have liquid corpus with your HUF, you can plan to take loan from HUF and pay interest to HUF. This way you will be getting deduction of interest from your income from Business or Profession where your tax bracket may be as high as 30% and on the other hand it becomes income of the HUF where your tax bracket may be as low as 0% or 10% depending on other income in the HUF head.

HUF can also take Loan :

- HUF can also take Loan. The loan taken can be invested in any asset to generate further income and the income which is generated from that asset will become income of HUF and will be taxed in the return of HUF income.

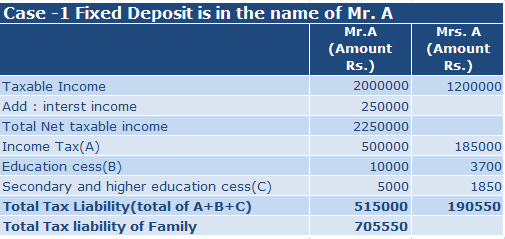

- If an Individual has corpus in his individual file and that is invested in any asset in individual name then income from that asset will be taxed under the income of that individual but if that individual transfers that corpus to his own HUF file in the form of loan and then invest in any asset like fixed deposit , property or any other kind of asset then income generated in the form of interest or rent or any other form will not be clubbed in the income of an individual. For example, if Mr.A has a corpus of Rs. 25 Lakhs in the name of individual which he wants to invest in Fixed deposit or Mutual funds or in property then income from these assets in the form of interest or rent or capital gain will become income of Mr.A in his individual head and if he is falling in higher tax brackets like 20% or 30% his tax liability will be very high on that income and his post tax income will be very low. But if he gives this corpus of Rs. 25 Lakhs as loan to Mr.A (HUF) and Mr.A (HUF) then invests this income in fixed deposit or mutual fund or property in the name of Mr.A (HUF) then income from these assets in the form of interest or dividend or capital gain or rent will be taxed in the hands of Mr. A (HUF) where tax slabs may be as low as 0% or 10%. So total tax liability of Mr. A and Mr. A( HUF) will be less then total tax liability of Mr.A if it is directly invested in the name of Mr.A. This is shown in the below chart.

For example family of Mr.A consists of Mr.A, Mrs.A and two children.

Case -1- Fixed Deposit in the name of Mr.A :Where Mr. A has net taxable income of Rs. 20 Lakhs and Mrs. A Has net taxable income of Rs. 12 Lakhs. Corpus of Rs. 25 Lakhs is invested in a 10% fixed deposit in the name of Mr. A which adds an additional income of Rs. 250000 in the Net taxable income of Mr.A. His total tax Liability would be as under.

Case -2 Fixed Deposit is in the name of Mr. A(HUF): Mr.A gives loan to Mr.A (HUF) and then Mr. A(HUF) makes fixed deposit .

It is clearly visible that there is significant tax saving of Rs. 77250 and this will continue for subsequent years also.

HUF can receive Inherited Assets: This is one of the very good tax planning points. Whatever inheritance is received in HUF is free from Tax and any subsequent income from such assets will be considered income of HUF and will not be considered income of individual. So in such case one can plan his inheritance to be received in such a way that he can receive it in HUF and in such case subsequent income from such inherited assets will become income of HUF.

HUF can receive Gifts :

- Gift from Relatives: As per section 56(2)(vi) of Income Tax Act any sum received by HUF in Cash or in kind, exceeding Rs.50000/- in a financial year without any consideration from anyone other than relatives is taxable. But if your HUF doesn’t have any other income and it receives a gift of Rs.250000 from a person other than relatives(members) it is taxable but as it is up to basic exemption limit of Rs.250000 it will become tax free and there will be not tax liability.

- For HUF relatives are the members of HUF: So any gift received by HUF from members of HUF exceeding Rs.50000 in a financial year either in cash or in kind is free from tax.

- Gits given to members and others by HUF : Gifts given to members and others by HUF will be taxable if exceeds Rs.50000 in a financial year in the hands of person who receives gift.

♦ What HUF cannot do?

- HUF cannot receive salary Income : HUF cannot receive salary income because it cannot perform any duties.

- HUF cannot open PPF Account : HUF can’t open PPF account. In May 2005, the government passed a rule PREVENTING HUFs from opening new accounts in the Public Provident Fund. All existing accounts, which had completed 15 years since the initial deposit, were also to be closed by 31 March 2011.

- HUF cannot run a Profession : One cannot run a professional practice in the name of HUF. Every profession requires an academic qualification and professional expertise in a particular area. HUF cannot have that academic qualification or professional expertise so it cannot run a profession. A good illustration of this is a Doctor, a Doctor cannot run his practice in the name of HUF.

♦ Clubbing of Income :

- Income from property (movable or immovable) converted from members to HUF in the form of Gift will be clubbed in the income of Individual. So if a member gifts something to HUf then in that case gift is exempted income for HUF but any income generated from that gift in the form of interest, rent or any other form will be clubbed in the income of member of HUF who gifted the basic asset. In this case even after partition of HUF, if spouse of such individual member who gifted property to HUF derives some income from such gifted property then that will be clubbed in the income of that individual member.

- But if above case if the member has given loan to HUF and then that money is invested in any asset and subsequently some income is generated from that income. In this case income will not be clubbed in the income of individual member even though the loan is interest free loan.

z♦ Conclusion : To conclude with HUF is a good tax planning tool which is generally underutilized by most of the people and therefore one should focus upon it. When you are planning structure of your business or profession or income from any other sources or house property, you should also keep taxation in mind and try to involve HUF in such a manner that it splits your income either from business income or from income from other sources. In my next article i will be writing on other legal aspects and disadvantages of HUF.